What Content Works for Skeptical CFOs? (And What They See Through Immediately)

Content that works for skeptical CFOs leads with verified financial outcomes, not features or benefits. The most effective types are: ROI case studies with specific, auditable numbers from named peer companies; third-party analyst validation; total cost of ownership models the CFO can stress-test themselves; and risk reduction proof rather than upside promises. CFOs distrust self-promotional vendor content by design and respond instead to evidence they didn't get directly from the vendor.

A VP of Sales sends the CFO your best case study. It's polished, the numbers are good, and the customer story is compelling. The CFO reads the executive summary, notes it was produced by your company, and files it. Two weeks later, they ask the champion: "Has anyone who actually uses this seen the return they claim?" The case study existed. The trust it needed didn't.

CFOs sign 79% of B2B deals, which means getting past a skeptical CFO isn't a sales edge. It's a baseline requirement for closing. The challenge is that CFOs are trained, by education and professional experience, to distrust vendor-produced claims. They understand that a vendor-produced case study, a vendor-produced ROI calculator, and a vendor-produced white paper all carry an incentive structure that makes every number suspect. The content that works for skeptical CFOs isn't better marketing. It's a fundamentally different type of evidence: peer-verified, third-party endorsed, financially specific, and structured to survive the kind of scrutiny a CFO applies to a capital allocation decision. This guide covers exactly what that content looks like and how to get it in front of the right person at the right stage.

Start with: 13 Most Important Types of Sales Enablement Content for the full content inventory that CFO-facing materials sit within.

Why CFOs Are Skeptical By Design (And Why That's Not a Bug)

CFOs are skeptical of vendor content because their professional function is to find the gap between what a vendor promises and what is verifiable. They are paid to protect capital from bad allocation decisions. A CFO who accepts vendor ROI claims at face value is doing their job badly. Skepticism is a feature of the role, not an obstacle to overcome. Content designed to work within that skepticism outperforms content designed to bypass it.

The Structural Reason

CFOs are trained to evaluate claims against independent evidence. Their professional function is to protect capital from bad allocation decisions. When a CFO sees a vendor-produced ROI calculator with a 40% cost-reduction headline, they apply a mental discount based on one known fact: the vendor has an incentive to select the most favorable number, choose the most favorable customers, and write the most favorable framing. The CFO isn't being difficult. They're doing their job. Content designed to argue the discount away will fail. Content designed to provide evidence that survives the discount will succeed.

What the Discount Looks Like in Practice

A vendor-produced case study will be read with a different assumption than a peer conversation, an analyst report, or an independently verified ROI calculation. The CFO applies a credibility weighting to every source. Peer companies who have already implemented: high credibility, no vendor stake. Third-party analysts (Gartner, Forrester, IDC): high credibility, independent methodology. Vendor-produced testimonials from unnamed customers: low credibility, selection bias visible. Vendor-produced ROI calculators with locked inputs: low credibility, optimism visible. The content that moves a skeptical CFO sits in the first two categories, not the last two.

The Specific Signals CFOs Weight and Discount

What CFOs discount:

- Testimonials without named companies or specific numbers

- 'Up to X%' performance claims without methodology

- Feature lists without financial outcomes

- Case studies from industries or company sizes that don't match the CFO's context

- Content that shows only upside without addressing implementation risk or cost

What CFOs weight more heavily:

- Quantified outcomes expressed in financial terms: payback period, cost reduction in dollars, headcount equivalent, revenue attributed

- Evidence from peer companies in comparable situations (same industry, same revenue range, similar organizational complexity)

- Third-party validation from sources without a direct stake in the vendor's sale

- Risk reduction framing alongside opportunity framing

Sales Enablement Collateral covers the full collateral landscape that CFO-stage materials are drawn from.

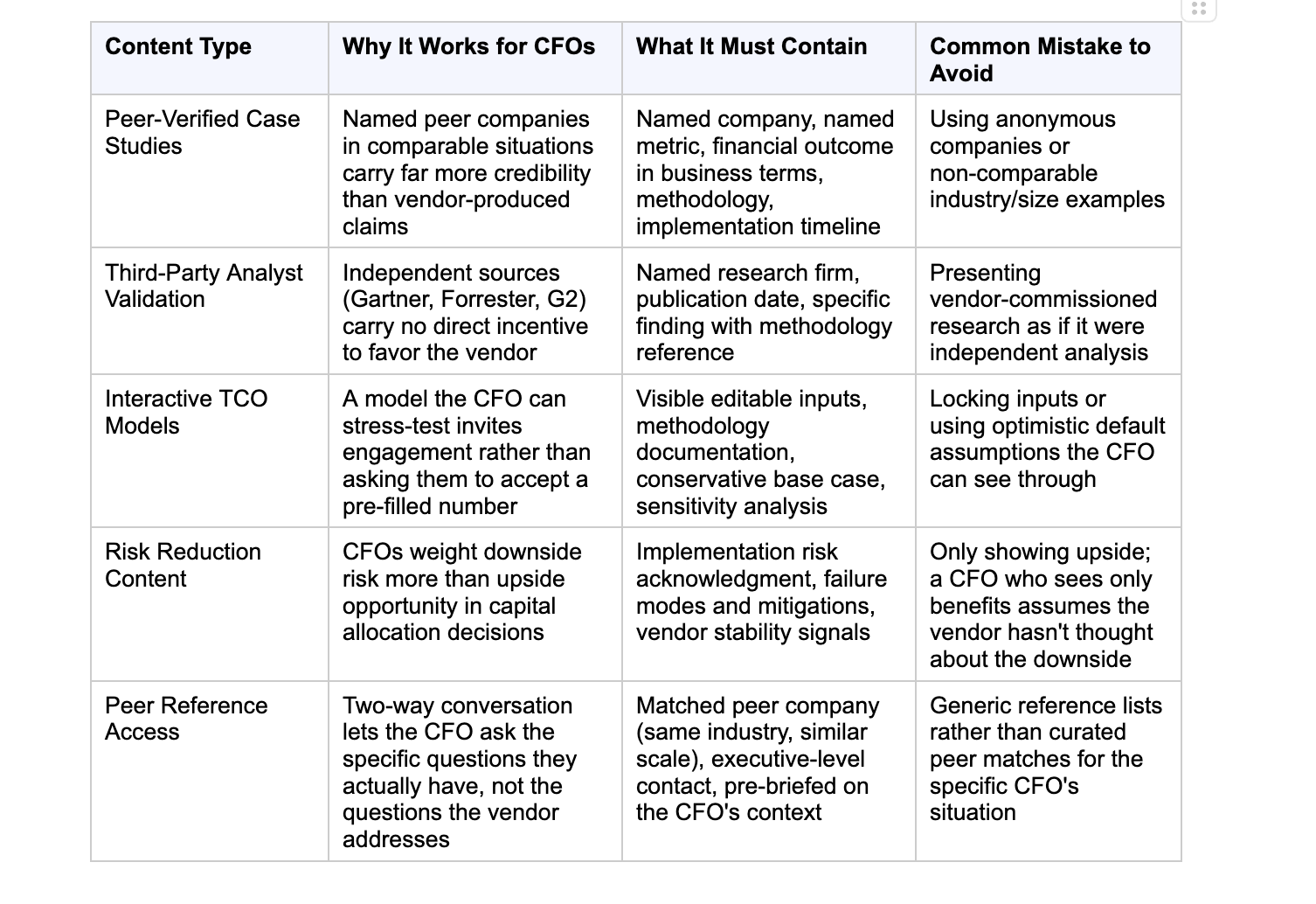

The Five Content Types That Actually Move a Skeptical CFO

The five content types that move skeptical CFOs are: peer-verified case studies from named companies with auditable financial outcomes; third-party analyst validation from firms without a vendor stake; interactive TCO models the CFO can stress-test; risk reduction content that acknowledges implementation failure modes; and peer reference access that lets the CFO ask their specific questions rather than reading the vendor's framing.

Here's what each type looks like done well, and what undermines it.

1. Peer-Verified Case Studies (Not Vendor-Produced Testimonials)

The most effective CFO-facing content is a case study from a company the CFO considers a peer: same industry, comparable revenue range, similar organizational complexity. The CFO is asking one question: did this work for someone who is actually like us? A case study from a Fortune 500 company presented to a 200-person SaaS CFO isn't evidence. It's noise. The size mismatch makes the financial comparison structurally irrelevant.

What makes a case study CFO-grade:

- Named company, named executive, named metric: not 'a leading software company saved 30%'

- Specific financial outcomes expressed in business terms: payback period, cost reduction in dollars, headcount equivalent saved, or revenue attributed

- Methodology explanation: how was the result measured, over what period, with what baseline

- Honest acknowledgment of the implementation timeline and any costs not included in the ROI figure

The structure that works follows the same logic as the best B2B case studies: lead with the specific problem the company faced, establish how that problem was costing them money before the solution, show the intervention, then deliver the outcome in auditable financial terms. Personalized, specific content gets read longer and shared internally more often than generic proof, which is the signal a CFO is evaluating even before they consciously decide to advocate for the purchase.

2. Third-Party Analyst and Research Validation

CFOs are trained to distinguish primary source from secondary source. A vendor saying "our customers see 40% cost reduction" is a primary source with obvious incentive. Gartner, Forrester, IDC, or McKinsey saying "organizations using this category of solution see 30 to 45% operational efficiency gains" is a secondary source without a direct stake in the vendor's sale. The credibility differential is structural, not stylistic.

Third-party content that works:

- Gartner Magic Quadrant placement references, cited from the Gartner publication, not a vendor press release

- Forrester Wave scores with the relevant evaluation criteria surfaced

- IDC research reports with their methodology and sample size disclosed

- G2 or TrustRadius benchmark reports aggregating real user outcomes across multiple vendors

What to avoid:

- Vendor-commissioned research presented as if it were independent analysis

- Research that doesn't disclose the vendor relationship or funding source

- Analyst quotes pulled from context to imply an endorsement the analyst didn't make

3. Total Cost of Ownership (TCO) Models the CFO Can Stress-Test

An ROI calculator the CFO cannot interrogate is a marketing artifact. A TCO model with editable inputs, visible methodology, and conservative default assumptions that the CFO can adjust is a financial analysis tool. One is promotional. The other invites active engagement from the most analytical person in the buying committee.

What makes a TCO model CFO-grade:

- All inputs visible and editable, not locked or hidden behind a sales form

- Baseline methodology explained: where the default numbers come from and why they were chosen

- Scenario comparison: current-state cost vs. proposed-state cost, including implementation costs and change management

- Conservative base case, not optimistic projections

- Sensitivity analysis: what happens to the outcome if the CFO adjusts the key assumptions down by 50%

A CFO who participates in building the financial model is far more likely to defend it to the board than a CFO who receives a completed calculation and is asked to sign off on someone else's math.

4. Risk Reduction Content (Not Just Upside Promises)

CFOs weight downside risk more heavily than upside opportunity in most capital allocation decisions. This is not the same thing as being conservative or resistant to change. It's a rational response to having responsibility for capital that took real effort to accumulate. A vendor who shows only upside is signaling they haven't thought seriously about the downside. A vendor who explicitly addresses risk, implementation failure modes, common adoption challenges, and what mitigation looks like, is demonstrating the rigor a financial executive recognizes.

Risk reduction content that works:

Implementation risk guides that acknowledge what can go wrong and how it's managed

Vendor financial stability signals: reference customers, years in operation, audit credentials

Contract structure explanations that clarify what the CFO is committing to and under what conditions they can exit

5. Peer Reference Access (Not Just Written Case Studies)

Written case studies are one-directional. The CFO reads the vendor's framing. A peer reference, an actual conversation between the CFO and a customer who went through the same decision, is two-directional. The CFO can ask the specific questions they actually have. The peer can answer in the financial language the CFO recognizes. This is the highest-value CFO conversion tool available, and it's not a piece of content in the traditional sense. It's a curated access arrangement that the content program enables.

The key is curation: a generic "reference list" is far less effective than a specifically matched peer company selected for industry, revenue range, and the CFO's known concerns. A CFO who speaks to a peer who faced the exact challenge they're worried about gets more signal from that 20-minute call than from every case study in the library.

Here's a quick-reference summary of all five types:

Sales Collateral: 17 Must-Have Types with Examples covers where CFO-facing assets fit within the broader collateral structure.

What Format CFO Content Needs to Be In

CFO-facing content needs a one-page executive summary that stands alone, a maximum of four pages total (one summary, two evidence pages, one methodology and sources page), financial data presented visually with a headline metric in a call-out box, and a format designed for the CFO's reading pattern: executive summary first, numbers before narrative, methodology as a credibility check. If the content requires scrolling or reading more than four pages to find the key financial claim, it won't get the attention it needs.

The CFO Reading Pattern

CFOs skim. They read the executive summary first. They go to the numbers before they read the narrative. They look for methodology and sourcing as a credibility check before they invest time in the full document. Content formatted for a practitioner, with a compelling narrative arc that builds to a headline number on page eight, fails with a CFO who will never reach page eight. Format should be designed for the reading behavior of the actual audience, not for the storytelling preference of the content creator.

The Executive Summary Rule

Every piece of CFO-facing content, regardless of type, needs a one-page executive summary that stands alone. The CFO will often share the summary with their team or reference it in a leadership meeting without having the underlying document in front of them. If the summary doesn't contain the key financial claims and their sources, it doesn't function as a standalone communication. If someone had to look up the full document to understand what the summary was saying, the summary wasn't written for a CFO.

Visual Data Over Tables

Financial data presented as a bar chart with a single headline number in a call-out box is more effective than the same data in a table buried in paragraph four. CFOs are comfortable with financial tables, but the visual presentation allows the headline metric to register before the CFO decides whether to read the methodology. A case study that leads with "40% cost reduction in 9 months" in a large call-out box, supported by the full methodology in the body, is more effective than a case study that buries the headline in paragraph four for the careful reader who makes it that far.

The Four-Page Maximum

A CFO-facing document longer than four pages will not be read in full under typical decision-making conditions. Budget one page for the summary, two pages for the evidence, one page for methodology and sources. Everything else goes in an appendix that the CFO can access if they want additional detail. If the argument can't be made in four pages, the argument hasn't been tightened enough. Length signals that the author didn't do the work of prioritizing what matters.

How to Build a CFO-Proof Content Sequence

Present ROI to a skeptical CFO in four stages: before the first CFO meeting, establish the financial framing through the champion so the CFO enters the conversation already thinking in financial terms; lead the first CFO interaction with a peer case study, not a product presentation; mid-evaluation, use an interactive TCO model the CFO can adjust; at the close, provide analyst validation and peer reference access. Each stage addresses a specific layer of CFO skepticism rather than trying to overcome it all at once.

Individual content assets matter. The sequence in which they're shared matters more. A CFO who encounters a vendor-produced ROI calculator before they've heard the problem framed in financial terms by their own champion will dismiss it. The same calculator, shared after the CFO has already accepted the financial framing, functions as confirmation rather than persuasion.

Stage 1: Establish Financial Framing Before the First CFO Meeting

The champion needs to have established the financial framing before the CFO encounters vendor content. If the first thing a CFO sees is a vendor-produced ROI calculator with optimistic defaults, they'll discount it before reading the second line. If the CFO enters the conversation already having heard their champion describe the problem in financial terms, the vendor's peer case study becomes confirmation of a narrative the CFO already partially believes, rather than an unsolicited claim they're asked to take on faith. The champion's internal credibility prepares the ground for the vendor's evidence.

Stage 2: Lead the First CFO Interaction With Peer Evidence, Not Product

The first content a CFO should receive from a rep is evidence from a peer company, not a product presentation. Product features are irrelevant to a CFO who hasn't yet accepted the financial case for the investment. A CFO who sees a product demo before accepting the business case is evaluating the product against nothing in particular. A CFO who sees a peer case study first is evaluating the product against a financial outcome they find credible. Sequence determines what the CFO is measuring the product against.

Sales Content Management Guide covers the governance layer that keeps the CFO-stage content sequence organized and current.

Stage 3: Interactive TCO Model Mid-Evaluation

Once the CFO has established enough interest to engage more deeply, provide the TCO model as an active tool rather than a passive document. Walk through the inputs together rather than sending a pre-filled version. A CFO who participates in building the financial model defends it to their peers. A CFO who receives a completed calculation defends someone else's math. The rep who facilitates the TCO session becomes a financial partner in the decision rather than a salesperson presenting a pitch.

Stage 4: Third-Party Validation at the Close

Analyst validation and peer reference conversations close the credibility gap that remains at the final decision stage. By this point, the CFO has engaged with the financial case. The remaining skepticism is typically about vendor claims rather than the underlying business case. Third-party evidence addresses that specific concern: the CFO no longer needs to accept the vendor's framing because they have an independent source saying the same thing.

How to Build a Sales Enablement Strategy covers how CFO-stage content fits into the broader sales enablement architecture.

How to Know Whether Your CFO Content Is Actually Working

Most teams build CFO content and never find out whether the CFO engaged with it, which sections held their attention, or whether it was forwarded internally. Download counts don't reveal any of this. Engagement analytics do.

The Problem With Measuring CFO Content by Download

A CFO who downloads a case study has taken one action. A CFO who opens it, spends four minutes on the executive summary, and then forwards it to the COO before returning to spend eight minutes on the financial methodology has taken a qualitatively different action. Both register as one download in most tracking systems. Only section-level engagement analytics distinguish between them. And the distinction matters, because the CFO in the second scenario is two to three steps further along the advocacy path than the one in the first.

What CFO-Stage Engagement Data Looks Like

- The behavioral signals that indicate real CFO engagement, not passive exposure:

- Section-level read time on a shared case study: did the CFO skip to the methodology, or read the narrative? Did they spend the most time on the financial outcomes section or the implementation timeline?

- Forward events: who else in the organization received the document? A CFO forwarding content to the COO or the board is building internal consensus without telling the rep they're doing it

- Return visits: the CFO came back to the document without being prompted, the strongest buying signal in the engagement data set

- Time on financial sections vs. time on feature sections: if the CFO spent all their time in the ROI section, the feature content is taking up space that additional financial evidence could occupy

How Engagement Data Improves Future CFO Content

If CFO engagement data shows consistently low time on the executive summary but high time on the financial methodology section, the summary isn't carrying the financial argument effectively enough for the CFO to skip past it. If CFOs consistently skip the industry context section and go straight to the numbers, that section is taking up real estate that additional financial evidence could use. Behavioral data is more reliable than any survey because it reflects what CFOs actually do with the content, not what they say they would do with it in a focus group.

What is content tracking? Types, Techniques, and Tools covers the full content tracking framework that CFO engagement analytics sits within.

How Paperflite Helps Teams Build and Measure CFO-Stage Content

The content types in Section 2, the sequence in Section 4, and the measurement framework in Section 5 all require an infrastructure layer: a content platform that organizes CFO-facing assets by persona, tracks section-level engagement on shared documents, and connects content activity to deal outcomes. Here's how Paperflite handles each one.

Persona-tagged content library for CFO-stage assets. Paperflite's content library supports persona-based tagging, letting marketing and enablement teams organize CFO-specific assets (peer case studies, analyst reports, TCO models) separately from champion-facing and practitioner-facing content. A rep preparing for a CFO conversation filters by persona and deal stage to find the right case study for a healthcare CFO in the evaluation stage, rather than searching through a full library that mixes CFO, technical evaluator, and champion content. (Source: GetApp, verified June 2026.)

Section-level engagement analytics reveal what CFOs actually read. When a rep shares a CFO-facing content collection through Paperflite, the platform tracks section-level engagement: how long the CFO spent on the executive summary, whether they moved to the financial methodology, whether they forwarded the content internally. This is the measurement layer from Section 5: engagement data that distinguishes a CFO who skimmed from one who engaged with the financial argument. (Source: Capterra verified reviews, Gartner Peer Insights, June 2026.)

Multi-stakeholder forwarding detection surfaces the buying committee. When a CFO forwards shared content to a COO, procurement contact, or board member, Paperflite detects the new viewer and adds them to the engagement timeline. This is the forward event signal from Section 5: the rep learns the CFO is building internal consensus before the CFO says so in a meeting.

Content Revenue Intelligence connects CFO-facing assets to closed-won deals. Paperflite's Content Revenue Intelligence shows which specific assets appear most often in deals that included a CFO in the decision and resulted in a closed-won outcome. This is the pattern analysis from Section 5: the feedback loop that tells enablement teams which CFO content is driving revenue, not just engagement.

Pricing

Paperflite pricing starts at $30/user/month (Starter plan, minimum 5 users), including the core content hub, SEEK AI-powered search, and storage sync with Google Drive, SharePoint, and Dropbox. The Professional plan is $50/user/month, adding CRM integrations (Salesforce, HubSpot, Pipedrive, Freshsales), white labeling, SSO, and a dedicated Customer Success Manager. The Advanced plan is $60/user/month, adding digital deal rooms, predictive Deal Insights, and AI-powered content recommendations. Enterprise pricing requires a custom quote. Content Hub Operations: Strategies for Managing Effectively and Organize B2B Marketing Content in 8 Simple Steps cover the library governance that makes persona-tagged CFO content sustainable.

See how Paperflite tracks which CFO-facing content actually moves deals. [Book a demo]

Conclusion

Skeptical CFOs don't respond to better marketing. They respond to better evidence. The distinction determines which content you build, how you structure it, and when in the deal you share it.

Peer case studies from named companies with auditable outcomes. Third-party analyst validation that doesn't carry a vendor sponsorship. TCO models the CFO can stress-test. Risk reduction framing that acknowledges what can go wrong. Peer reference access that doesn't require the CFO to take the vendor's word for anything. These are the content types that move a CFO from skeptical to signed.

And the teams that can track which specific asset, shared at which specific stage, appears in their closed-won CFO deals are the ones building the next generation of that content from data rather than intuition. That's the compounding advantage: not just creating better CFO content, but knowing which CFO content is actually working.

Buyer Persona Importance: Are You Talking to the Right Prospect? connects the CFO persona to the broader buyer persona framework. And 7 Key Benefits of Sales Enablement You Can't Afford to Miss shows where CFO-stage content fits within the full revenue impact of sales enablement.

Ready to build the content library that actually wins CFO sign-off? [Talk to the team]

Frequently Asked Questions

Why are CFOs skeptical of vendor-produced content?

CFOs are professionally trained to evaluate capital allocation decisions against independent evidence. Their function is to find the gap between what a vendor promises and what is verifiable. Vendor-produced case studies, white papers, and ROI calculators carry an inherent credibility gap because the CFO knows the vendor selected favorable examples, used optimistic assumptions, and controlled the framing. Skepticism is a feature of the CFO role, not an obstacle. Content designed to provide evidence the CFO can verify independent of the vendor is more effective than content designed to argue the skepticism away.

What type of content do CFOs respond to most?

CFOs respond most to evidence they didn't get directly from the vendor: peer case studies from named companies with specific, auditable financial outcomes; third-party analyst validation from firms without a direct stake in the vendor's sale; and interactive TCO models where the CFO can stress-test the assumptions rather than accepting a pre-filled calculation. Content that leads with risk reduction alongside upside opportunity also performs well, because it demonstrates financial rigor rather than promotional optimism.

What does a CFO want to see in a business case?

A CFO wants to see: a specific financial outcome expressed in the terms they use to evaluate capital allocation (payback period, cost reduction in dollars, headcount equivalent, revenue attributed); the methodology behind that outcome (how it was measured, over what period, with what baseline); evidence from a peer company in a comparable situation; acknowledgment of implementation costs and risks; and validation from a source independent of the vendor. What they don't want: testimonials without specific numbers, feature lists without financial outcomes, or ROI claims without methodology.

How do you present ROI to a skeptical CFO?

Present ROI in stages rather than all at once. Before the first CFO meeting, establish the financial framing through the champion so the CFO enters the conversation already thinking in business terms. Lead the first CFO interaction with a peer case study from a named company, not a product presentation. Mid-evaluation, use an interactive TCO model the CFO can adjust rather than a pre-filled calculation. At the close, provide analyst validation and peer reference access. Each stage addresses a specific layer of CFO skepticism rather than attempting to overcome it all in a single presentation.

What format should CFO-facing content be in?

CFO-facing content needs a one-page executive summary that stands alone, a maximum of four pages total, and financial data presented visually with a headline metric in a call-out box. The format should be designed for the CFO's actual reading pattern: executive summary first, numbers before narrative, methodology as a credibility check. If the content requires scrolling or reading more than four pages to find the key financial claim, it won't get the engagement it needs from a CFO who applies the same efficiency standards to reading as to capital allocation.

How do you build credibility with a CFO buyer?

Credibility with a CFO comes from four sources: named peer evidence from a real company of comparable size and industry with auditable outcomes; independent third-party validation from analyst firms or aggregated review platforms without a vendor stake; transparent methodology showing exactly how outcomes were measured; and honest risk acknowledgment addressing what can go wrong rather than only showing upside. Credibility is not built through more polished marketing. It's built by providing evidence the CFO can verify without taking the vendor's word for it.

How do you know if CFO-facing content is actually working?

Track section-level engagement on shared CFO content: how long did the CFO spend on the executive summary versus the financial methodology, did they forward the document internally, did they return without being prompted. These behavioral signals show whether the CFO engaged with the financial argument or skimmed and moved on. At the library level, track which assets appear most often in deals that included a CFO and closed. The combination of asset type, deal stage, and outcome identifies which CFO content is actually driving revenue rather than just being shared.

Should CFO content be different from champion content?

Yes, significantly. Champion content needs to explain how the product works, establish the use case, and build internal conviction for the investment. CFO content assumes the champion has already done that work. The CFO doesn't need to understand the product; they need to evaluate the financial case for the investment. CFO content should skip product features almost entirely and focus on financial outcomes, peer evidence, and risk framing. Sending champion content to a CFO, or CFO content to a champion, signals the sales team hasn't segmented by stakeholder, which reduces credibility with both audiences.